Teach Your Teen How to be a Powerful Saver Now

For kids to have financial security, they need to learn how to be a powerful saver. It is an important life skill for teens to learn and the earlier they learn it, the more successful they will be financially.

A key component of managing money is saving, or systematically setting aside a portion of your income to cover emergencies and prepare for the future.

This post contains affiliate links.

Table of Contents

What are Your Middle Schoolers Learning About Personal Finance?

Most schools don’t teach personal finance. That means it’s up to us, the parents, to make sure our kids understand the basics of money management. That includes learning how to budget, spend smartly, and the importance of saving. Have you sat down and intentionally taught your teen how to do these three things? If not, they’re not only learning from watching what’s going on in the world, they’re learning by watching you. So, what are they learning, especially about saving?

Through our national debt, they learn that spending more than you make is the way to do business. If your debt continues to grow, you’re not saving anything. You’re borrowing against the future. Our teens are regularly taught that it’s okay to take on huge amounts of debt in order to get a college degree. Statistics show that college graduates are leaving with an average of $37,172 of student loans. Considering that in 2014 the average starting salary for a new college graduate was $48,127, they will have to set aside $351 (about 9%) of their income just to make that monthly payment. How can they possible save anything after paying that along with their other obligations like rent, utilities, gas, insurance, etc? They will be like millions of other college graduates who are foregoing saving for retirement as they work to pay down student loans.

And what are you teaching them about saving? Are you living paycheck to paycheck? Spending your check before it even arrives? Or are you setting aside money for emergencies?

Everyone Should Have an Emergency Fund

Another saying that I often heard from my grandparents was to “save for a rainy day.” If history tells us anything, it is that there will always be bumps in the road of life. Saving for those bumps won’t make them go away, but it can help them be more manageable. If you have money set aside for emergencies, you won’t have to borrow the money to cover the expense. Money that usually comes from a credit card company, which costs you more in the long run.

We have been teaching our daughters to save money for years. They each have a bank with three compartments labeled, give, save, and live. Whenever they earn money, they put at least 10% of it into the first two slots and the rest in the third. So, when emergencies come up, they can cover them.

For example, as Megan shared in her smart spending post, we have an agreement with our daughters regarding their cell phones. While we paid for the phones initially (and carry the insurance), they are required to pay for replacements out of their pockets. Well, our youngest recently broke the screen on her phone. She had 2 choices to make. She could either live without a phone or she could pay the insurance deductible from her savings and replace her phone all own her own. I’m sure you can imagine what she chose. But she only had that option because we taught her to save money for a rainy day.

Another example is a big one. As I mentioned, we’ve been teaching our kids how to save for years. Luckily, we’ve been living by our advice as well. A couple of weeks ago, I was laid off from my job of 11 years. I have been the sole breadwinner in the family since our oldest was born. Normally, this would send myself and our whole house into chaos and stress. But, because we have a fully funded emergency fund, we have breathing room. Is it ideal? No. But I can’t imagine what this transition would look like if we hadn’t been saving, preparing for something like this.

Saving for Retirement

Back to what your teens are learning from you. Are you teaching them to set aside at least 10% of their income for retirement? Or are you showing them that planning for the future isn’t important?

Sure, it’s more fun to get that shiny new car than save for something that’s decades away. But it is crucial that we teach our kids that saving for the future is essential. With fewer companies offering pensions and how frequently we change companies anyway, it’s up to each individual to prepare financially for retirement. Don’t let your kids fall into the false thinking that the government will take care of them. Don’t let them put their future in anyone else’s hands but their own. In order to do that, they need to start saving, and start early.

The habit of saving is itself an education; if fosters every virtue, teaches self-denial, cultivates the sense of order, trains to forethought, and so broadens the mind. – T.T. Munger

Starting Early Has a Huge Impact

One of the benefits of learning how to save early in life is the power of compound interest. That’s the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest. It is the result of reinvesting interest, rather than paying it out, so that interest in the next period is then earned on the principal sum plus previously accumulated interest.

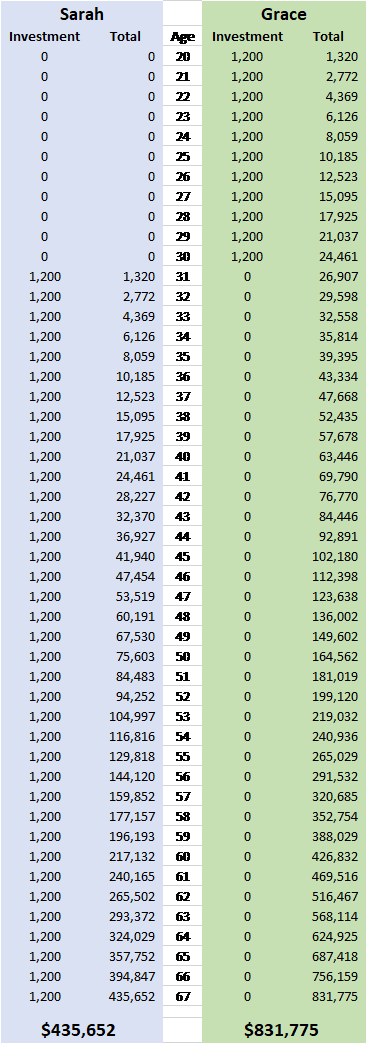

So if you want to see what that means, let’s look at a hypothetical situation. Sarah and Grace are identical twins. At age 20, they both have the ability to invest $1,200 a year. To keep the math simple, let’s assume an annual rate of return of 10%. The average annualized total return for the S&P 500 index over the past 90 years is 9.8 percent, so this is probably a fair estimate.

Sarah decides her expenses are too much and she can’t afford to save anything. Grace knows the importance of saving early and decides to cut back on her spending in order to make the investment in herself. Grace invests $1,200 a year until the age of 30 and then stops her yearly contribution. Sarah does not start saving regularly until she is 30 years old, but continues to invest $1,200 a year until retirement age of 67. Who do you think has more savings for retirement? My guess is most will say Sarah because she is saving longer, but you would be wrong.

The moral of the story? Encourage your teen to start saving early! Then they can leverage the power of compound interest. Grace invested only $13,200, and ends up with $831,775, while Sarah invested $44,400 and ends up with only $435,652. Because Grace started early, she comes out ahead by almost $400,000. That’s a powerful reason to make saving a priority.

Your teen may not be interested in retirement, but maybe they have a large purchase they’re thinking about. Perhaps a new computer, phone, or even a car. Most teens don’t earn enough money at one time to pay for bigger ticket items. That means they need to learn how to save money over time to reach a financial goal. In today’s world, delayed gratification is almost non-existent, but you can teach your teen that buying items that they’ve spent months (or years) saving for will often lead to greater pride in ownership. Things just means more when you work hard for them.

Learning How to Save Your Money Takes Practice

Finally, like any habit we are trying to establish we need to practice. Just like we go to the gym and work our muscles to build our strength and endurance, we need to teach our teens that personal finance is a muscle that must be practiced and exercised for us to be able to leverage it to the fullest. Grab a bank with three separate compartments to help make it easy for your teen to divide their money and practice money management. You don’t even have to go out and buy anything if you don’t want to. You can use three separate piggy banks or three mason jars with a slot cut in the lid. Just get your teen into the habit of separating their money into give, save, and spend.

Take the time to sit down with your teen to talk about the power of saving and encourage them to start saving early.

Important Personal Finance Fundamentals Teens Need to Know

My husband and I have put together some other things that we are doing in our family to make sure our girls become financially literate – personal finance fundamentals. We hope you’ll read along and share your experiences with us as we give you a glimpse into our lives.

- 2 Fun Board Games that Will Teach Teens About Money Management

- 50 Fantastic Ways for Teens to Make Money

- Teach Your Teen How to Make Smart Spending Decisions

- Teaching Teens How to Budget and Why It’s an Important Skill

Additional Money Management Resources

- Activities you can use to teach money management

- How to Turn $100 into $1,000,000: Earn! Save! Invest!

- I Want More Pizza: Real World Money Skills For High School, College, And Beyond

- KidsWealth Money Kit

- Not Your Parents’ Money Book: Making, Saving, and Spending Your Own Money

How are you teaching your teen to save?

Craig Zechman

Latest posts by Craig Zechman (see all)

- Martin Luther King Jr. Virtual Field Trips and Online Resources - February 5, 2021

- 20+ Alaska Virtual Field Trips That Tweens Will Love - January 28, 2021

- Teach Your Teen How to be a Powerful Saver Now - April 12, 2018

5 Comments

Comments are closed.